Introduction to Inflation

Inflation, a term frequently mentioned in economic discussions, is a phenomenon that affects individuals, businesses, and nations alike. It’s a concept that has been around for centuries, shaping the course of economies and influencing financial decisions. This section aims to provide a comprehensive understanding of inflation, its historical context, and its significance in the economic landscape.

Definition and Basic Concepts

Inflation is the rate at which the general level of prices for goods and services rises, causing purchasing power to fall. Essentially, when inflation rises, every dollar you hold buys a smaller percentage of a good or service.

Key Concepts:

- Price Level: Refers to the average of current prices across the entire spectrum of goods and services produced in the economy.

- Purchasing Power: The value of a currency expressed in terms of the amount of goods or services that one unit of money can buy. Inflation erodes purchasing power.

- Base Year: The year used for comparison in the measurement of inflation.

Comparison Table: Inflation vs. Deflation vs. Disinflation

| Term | Definition | Impact on Economy |

|---|---|---|

| Inflation | A rise in the general price level | Reduces purchasing power |

| Deflation | A decline in the general price level | Increases purchasing power but can lead to reduced spending |

| Disinflation | A decrease in the rate of inflation | Indicates slowing inflation but not necessarily negative inflation |

Historical Perspective on Inflation

Inflation is not a new concept. Ancient civilizations, including the Romans and Greeks, faced inflation when they produced more coins without the backing of gold or silver, leading to a decrease in the value of their currency.

The 20th Century: The world saw some of its highest inflation rates during this period. Notably, the hyperinflation in Germany post-World War I and in Zimbabwe in the early 2000s are stark reminders of how unchecked inflation can devastate an economy.

Modern Times: Central banks, like the Federal Reserve in the U.S., now have tools and policies in place to monitor and control inflation, aiming for a balance that promotes growth without letting inflation run rampant.

The Importance of Inflation in the Economy

Inflation plays a dual role in the economy. On one hand, moderate inflation is seen as a sign of a growing economy. On the other, high inflation can erode savings and destabilize the economy.

- Economic Growth Indicator: A moderate level of inflation typically indicates that an economy is growing. If demand for goods and services increases, prices tend to rise, reflecting this demand.

- Wage Adjustments: Inflation can influence wage negotiations. If workers expect prices to rise, they might demand higher wages, which can further fuel inflation.

- Monetary Policy: Central banks adjust monetary policy based on inflation. For instance, if inflation is too high, a central bank might increase interest rates to cool down the economy.

- Debt Relief: For borrowers, especially governments, inflation can reduce the real value of debt. If a government owes $1 million but then experiences inflation, the real value of that debt decreases.

However, unchecked and high inflation can lead to uncertainty in the economy, reduced purchasing power, and can even lead to economic recessions.

Understanding inflation is crucial for both individual financial planning and for policymakers guiding the economic direction of a nation. As we delve deeper into the subsequent sections, we’ll explore the intricate relationship between inflation and various economic facets, from investments to borrowing and lending.

How Inflation Erodes Investment Value

Inflation, often termed the “silent thief,” has a profound impact on investments. While it might not be immediately apparent, over time, the eroding effects of inflation can significantly diminish the real value of investments. This section delves into the mechanics of how inflation affects investment value and underscores the importance of considering inflation when making investment decisions.

The Real Value of Investment

At its core, the real value of an investment is what it’s worth after adjusting for inflation. It’s not just about the nominal returns (the percentage increase you see on paper) but the purchasing power that your investment holds.

Formula for Real Rate of Return:

For instance, if you have an investment that yields a 7% return in a year, but inflation for that year is 3%, the real rate of return is only 4%.

Loss in Spending or Purchasing Power

Inflation reduces the purchasing power of money. This means that with each passing year, a dollar can buy less than it could the previous year. For investors, this translates to a decrease in the real value of their returns.

Example:

Suppose you invest $1,000 in a fixed deposit that promises a 5% return after one year. At the end of the year, you’d have $1,050. However, if the inflation rate was 3% that year, the purchasing power of your $1,050 is equivalent to only $1,015.50 in the previous year’s dollars. Thus, your real profit is just $15.50, not the $50 it appears to be on paper.

The Need for Returns to Match or Exceed Inflation

For an investment to be truly profitable, its returns need to at least match the prevailing inflation rate. If the returns are below the inflation rate, the investor is effectively losing money in terms of purchasing power.

Comparison Table: Nominal vs. Real Returns

| Investment Type | Nominal Return | Inflation Rate | Real Return |

|---|---|---|---|

| Savings Account | 2% | 3% | -1% |

| Stock Portfolio | 8% | 3% | 5% |

| Bonds | 4% | 3% | 1% |

From the table, it’s evident that even if an investment like a savings account provides a positive nominal return, the real return can be negative once inflation is accounted for.

While inflation is an inevitable economic phenomenon, its impact on investments cannot be ignored. Investors need to be proactive in ensuring their portfolio’s returns not only match but ideally exceed the inflation rate. This is crucial to safeguard the real value of their investments and ensure long-term financial growth. The subsequent sections will delve deeper into strategies and asset classes that can help mitigate the effects of inflation on investments.

Inflation and Asset Classes

Inflation’s influence isn’t uniform across all asset classes. Some assets are more resilient to inflation, while others might suffer more pronounced effects. Understanding how different asset classes respond to inflation can help investors make informed decisions and diversify their portfolios effectively. This section classifies and examines the impact of inflation on various asset classes.

Effect on Liquid Assets

Liquid assets are those that can be quickly converted into cash without a significant loss in value. Common examples include savings accounts, money market funds, and certain short-term government bonds.

Impact of Inflation:

- Savings Accounts: Typically offer interest rates lower than the inflation rate, leading to a reduction in real value over time.

- Money Market Funds: While they might offer slightly better returns than savings accounts, they still often lag behind inflation, especially in high-inflation environments.

- Short-Term Government Bonds: These might offer a slightly higher yield than savings accounts, but in an inflationary environment, their real returns can be minimal or even negative.

Illiquid Assets and Their Natural Defense

Illiquid assets are those that cannot be quickly converted into cash without potentially incurring a significant loss. Real estate, art, and certain collectibles fall into this category.

Inflation’s Impact and Defense Mechanisms:

- Real Estate: Historically, real estate tends to appreciate at a rate that matches or exceeds inflation. This is because the replacement cost of buildings and land typically rises with inflation, pushing property values up.

- Art and Collectibles: The value of unique items like art can be more resistant to inflation because their worth isn’t solely tied to currency value. However, their value can be subjective and influenced by trends and demand.

- Precious Metals: Gold, silver, and other precious metals have historically been seen as a hedge against inflation. Their value often rises when confidence in fiat currencies diminishes.

Inflation-Protected Securities (TIPS)

Treasury Inflation-Protected Securities (TIPS) are government bonds specifically designed to protect investors from inflation. The principal value of TIPS rises with inflation and falls with deflation.

How TIPS Work:

- Principal Adjustment: The bond’s principal is adjusted based on changes in the Consumer Price Index (CPI). If inflation is 2% in a year, a $1,000 TIPS would have its principal adjusted to $1,020.

- Interest Payments: Interest is paid on the adjusted principal. So, if the bond pays 1% interest, the payment would be based on the adjusted $1,020 principal, not the original $1,000.

- Maturity: Upon maturity, investors receive either the original or the inflation-adjusted principal, whichever is higher.

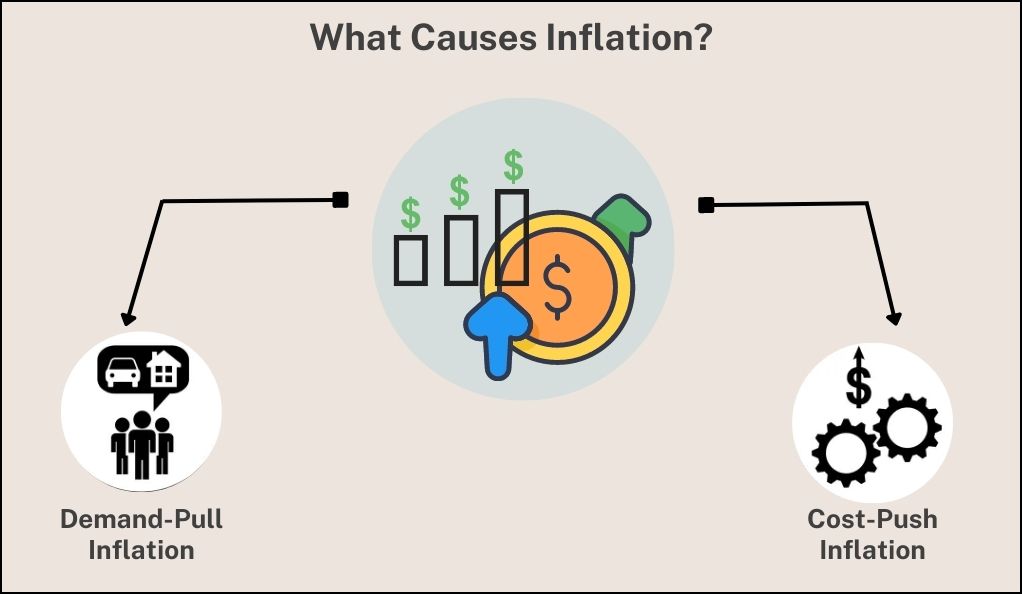

What Causes Inflation?

Inflation, while a common economic phenomenon, is driven by a myriad of factors. These factors can be broadly categorized into demand-side causes, supply-side causes, and institutional factors. Understanding the root causes of inflation is crucial for policymakers and investors alike, as it aids in predicting future trends and formulating strategies to mitigate its effects. This section elucidates the primary causes of inflation.

Demand-Pull Inflation

This type of inflation occurs when the demand for goods and services exceeds their supply in an economy. It’s essentially a result of an imbalance between demand and supply.

Key Drivers:

- Increased Consumer Spending: Often fueled by lower interest rates, increased consumer confidence, or government fiscal policies.

- Economic Growth: Rapid economic expansion can lead to increased spending and investment.

- External Factors: Such as increased demand for exports or foreign investment.

Cost-Pull Inflation

Cost-pull inflation is the result of rising production costs leading to decreased supply. When it becomes more expensive to produce goods and services, producers often pass on these costs to consumers in the form of higher prices.

Key Drivers:

- Rising Labor Costs: If wages increase faster than productivity, it can lead to higher production costs.

- Increased Prices of Raw Materials: Such as oil, metals, or agricultural products.

- Supply Chain Disruptions: Natural disasters, geopolitical tensions, or pandemics can disrupt supply chains, leading to increased costs.

Government’s Role in Controlling Inflation

Governments and central banks play a pivotal role in either exacerbating or mitigating inflation through their policies.

Key Factors:

- Monetary Policy: Central banks can influence inflation through tools like interest rates. Raising interest rates can cool down an overheated economy and reduce spending.

- Fiscal Policy: Government spending and taxation policies can influence demand. For instance, increased government spending can boost demand, potentially leading to demand-pull inflation.

- Currency Value: Governments can influence their currency’s value. A weaker currency can make imports more expensive, contributing to cost-pull inflation.

- Regulation and Price Controls: Direct interventions, like setting price ceilings or subsidies, can influence prices, though they can also lead to shortages or surpluses.

Inflation is a multifaceted phenomenon with various underlying causes. While some factors are inherent to economic cycles, others can be influenced by policy decisions. Recognizing these causes is the first step in crafting strategies to navigate inflationary environments, whether you’re a policymaker aiming to stabilize an economy or an investor looking to protect your assets. The subsequent sections will delve deeper into the relationship between inflation and other economic entities, such as borrowers and lenders.

Inflation’s Impact on Borrowers and Lenders

Inflation doesn’t just influence the value of money; it also affects the dynamics between borrowers and lenders. While borrowers might see some benefits in an inflationary environment, lenders often face challenges. This section delves into the nuanced relationship between inflation, borrowing, and lending, highlighting the advantages and disadvantages for both parties.

How Inflation Benefits or Harms Both Parties

Inflation can be a double-edged sword when it comes to borrowing and lending. Here’s a breakdown of its impact:

Borrowers:

- Advantages:

- Reduced Real Debt Burden: The real value of debt diminishes with inflation. If a borrower took a loan of $100,000 at a fixed interest rate and inflation rises, the real value of that debt in terms of purchasing power decreases over time.

- Fixed Interest Rates: If a borrower has a loan with a fixed interest rate, inflation can make the future payments cheaper in real terms.

- Disadvantages:

- Variable Interest Rates: Loans with variable or adjustable interest rates might see rate hikes in inflationary environments as lenders try to compensate for the reduced purchasing power of future repayments.

- Tighter Credit Conditions: In high inflation scenarios, lenders might become more risk-averse, making it harder to secure loans.

Lenders:

- Advantages:

- Higher Interest Rates: In an attempt to combat inflation and protect their returns, lenders might increase interest rates, especially on variable-rate loans.

- Collateral Appreciation: If a loan is secured against an asset like property, the value of that collateral might rise with inflation, offering better security for the lender.

- Disadvantages:

- Eroded Real Returns: For fixed-rate loans, the real value of the repayments received from borrowers diminishes with inflation.

- Default Risk: High inflation can strain borrowers, increasing the risk of defaults.

The Relationship with Interest Rates

Central banks often adjust interest rates in response to inflation. Here’s how it impacts borrowers and lenders:

- Rising Interest Rates: Central banks might increase rates to combat high inflation. This can make borrowing more expensive and saving or lending more attractive.

- Falling Interest Rates: In low inflation or deflationary scenarios, central banks might reduce rates to stimulate spending and borrowing.

Comparison Table: Inflation’s Impact on Borrowers vs. Lenders

| Aspect | Borrowers | Lenders |

|---|---|---|

| Real Debt Value | Decreases with inflation | Real value of repayments decreases |

| Interest Rates (Fixed) | Payments become cheaper in real terms | Real returns diminish |

| Interest Rates (Variable) | Risk of rate hikes | Can adjust rates to protect returns |

| Credit Conditions | Might face stricter borrowing conditions | Might impose stricter lending criteria |

| Collateral | Can borrow against appreciating assets | Have better security with appreciating collateral |

| Default Risk | Increased strain might lead to defaults | Face higher risk of borrower defaults |

Inflation reshapes the landscape of borrowing and lending. While it might offer some advantages, the challenges it poses necessitate careful financial planning and strategy. Both borrowers and lenders need to be aware of the prevailing inflationary environment and adjust their decisions accordingly. The upcoming sections will further explore strategies to shield investments from the effects of inflation and delve into emerging trends in the financial world.

Strategies to Protect Investments from Inflation

Inflation, often dubbed the “silent thief,” can erode the real value of investments over time. However, with strategic planning and diversification, investors can shield their portfolios from the adverse effects of inflation and even capitalize on the opportunities it presents. This section outlines various strategies that investors can employ to protect and grow their investments in the face of inflation.

Investing in Stocks, Bonds, and Mutual Funds

- Stocks: Historically, equities have provided a hedge against inflation. Companies can often pass on increased costs to consumers, which can lead to higher revenues and potentially higher stock prices.

- Bonds: Traditional bonds might lose value during inflationary periods due to their fixed interest payments. However, inflation-linked bonds or TIPS can offer protection as their principal adjusts with inflation.

- Mutual Funds: Diversified mutual funds, especially those focusing on equities or commodities, can offer a hedge against inflation. Some funds are specifically designed to counteract inflationary pressures.

Converting Liquid Assets

Liquid assets, like cash or money market funds, are most vulnerable to inflation. Converting them into assets that have a better chance of outpacing inflation can be a wise move.

- Real Estate: Property often appreciates over time, making it a good hedge against inflation.

- Precious Metals: Gold and silver have historically been seen as safe havens during inflationary periods.

- Commodities: Investing in commodities like oil or agricultural products can be beneficial as their prices often rise with inflation.

Utilizing Inflation-Indexed Bonds

Inflation-Indexed Bonds, such as TIPS in the U.S., are designed to protect investors from inflation. The principal of these bonds is adjusted based on inflation, ensuring that the investor’s returns keep pace with the rising cost of living.

Diversification

One of the cardinal rules of investing is diversification, and it holds especially true in the face of inflation.

- Geographical Diversification: Investing in international markets can provide a hedge, especially if one’s home country is experiencing high inflation.

- Asset Diversification: Spreading investments across various asset classes can reduce the risk associated with inflation. For instance, a mix of equities, real estate, and commodities can offer a balanced approach.

A Gap in the Market: Inflation and Emerging Investment Platforms (Interesting Gap)

In the ever-evolving financial landscape, new investment platforms and strategies continually emerge, offering innovative solutions to age-old challenges. One such challenge is inflation. As traditional investment avenues sometimes fall short in providing adequate protection against inflation, the market sees the rise of novel platforms and strategies. This section delves into the intersection of inflation and these emerging investment platforms, highlighting their role, case studies, and future trends.

The Role of Fintech in Inflation Management

Fintech, or financial technology, has revolutionized the way we approach finance. From digital banking to robo-advisors, fintech solutions offer a fresh perspective on managing inflation.

- Digital Assets and Cryptocurrencies: Digital currencies like Bitcoin are often touted as “digital gold” and a hedge against inflation. Their decentralized nature and limited supply make them an attractive option for some investors during inflationary periods.

- Robo-Advisors: These automated platforms use algorithms to provide investment advice. They can quickly adjust portfolios based on inflationary trends, ensuring optimal asset allocation.

- Peer-to-Peer Lending: By connecting borrowers directly with lenders, P2P platforms can offer better interest rates, potentially outpacing inflation.

Future Trends and Opportunities

- Integration of AI in Investment: As artificial intelligence becomes more sophisticated, we can expect AI-driven platforms that can predict inflationary trends and adjust investment strategies in real-time.

- Growth of Sustainable and Impact Investing: With increasing awareness of global challenges, there’s a rising trend in investing in sustainable projects that also offer protection against inflation.

- Expansion of Digital Assets: Beyond cryptocurrencies, we might see the rise of tokenized assets, from real estate to art, allowing fractional ownership and providing avenues to hedge against inflation.

- Global Investment Platforms: With the world becoming more interconnected, platforms that allow cross-border investments can offer diversification, spreading risks associated with inflation in any one region.

Conclusion

In the intricate tapestry of global economics, inflation stands out as a pivotal thread, influencing individual financial decisions, shaping business strategies, and guiding national policies. Through our exploration of this phenomenon, we’ve unearthed its multifaceted nature, from its foundational concepts to the innovative strategies designed to combat its effects. The ever-evolving financial landscape offers both challenges and opportunities in the face of inflation. However, armed with knowledge, diversification, and a willingness to adapt, investors can navigate these inflationary waters with confidence. As we move forward in this dynamic world of finance, it’s imperative to remain informed, embrace innovation, and view challenges like inflation not as insurmountable obstacles but as catalysts for growth and evolution.

At bitvestment.software, our commitment is to deliver unbiased and reliable information on subjects like cryptocurrency, finance, trading, and stocks. It's crucial to understand that we are not equipped to offer financial advice, and we actively encourage users to conduct their own comprehensive research.

Read More